Special Update: Iran and Long-Term Investing

Mar 2, 2026

March 2, 2026

As you have seen in the news, the U.S. and Israel have launched military strikes against Iran, targeting its leadership, military assets, and nuclear infrastructure. Iran’s Supreme Leader is confirmed to have been killed, and Iran has retaliated with missile and drone attacks across the Middle East. President Trump has stated that the goal of the operation, dubbed “Operation Epic Fury,” is regime change in Tehran, with strikes expected to continue for weeks and a number of U.S. troop casualties already reported.

The situation is evolving rapidly, and without taking away from the severity of these events and the human impact, investors will naturally have questions about what this means for markets, oil prices, and their portfolios.

President Dwight D. Eisenhower once said that “plans are worthless, but planning is everything.” Applied to today, the lesson is that specific geopolitical events are unpredictable, but the fact that they occur regularly is not. The process of structuring a portfolio and making financial plans is designed precisely to deal with this uncertainty. While each event is unique, financial markets have navigated countless wars, crises, and regional conflicts, including the U.S. operation in Venezuela earlier this year.

The key for long-term investors is to separate geopolitical headlines from portfolio decisions. What should investors keep in mind as events unfold in the coming weeks?

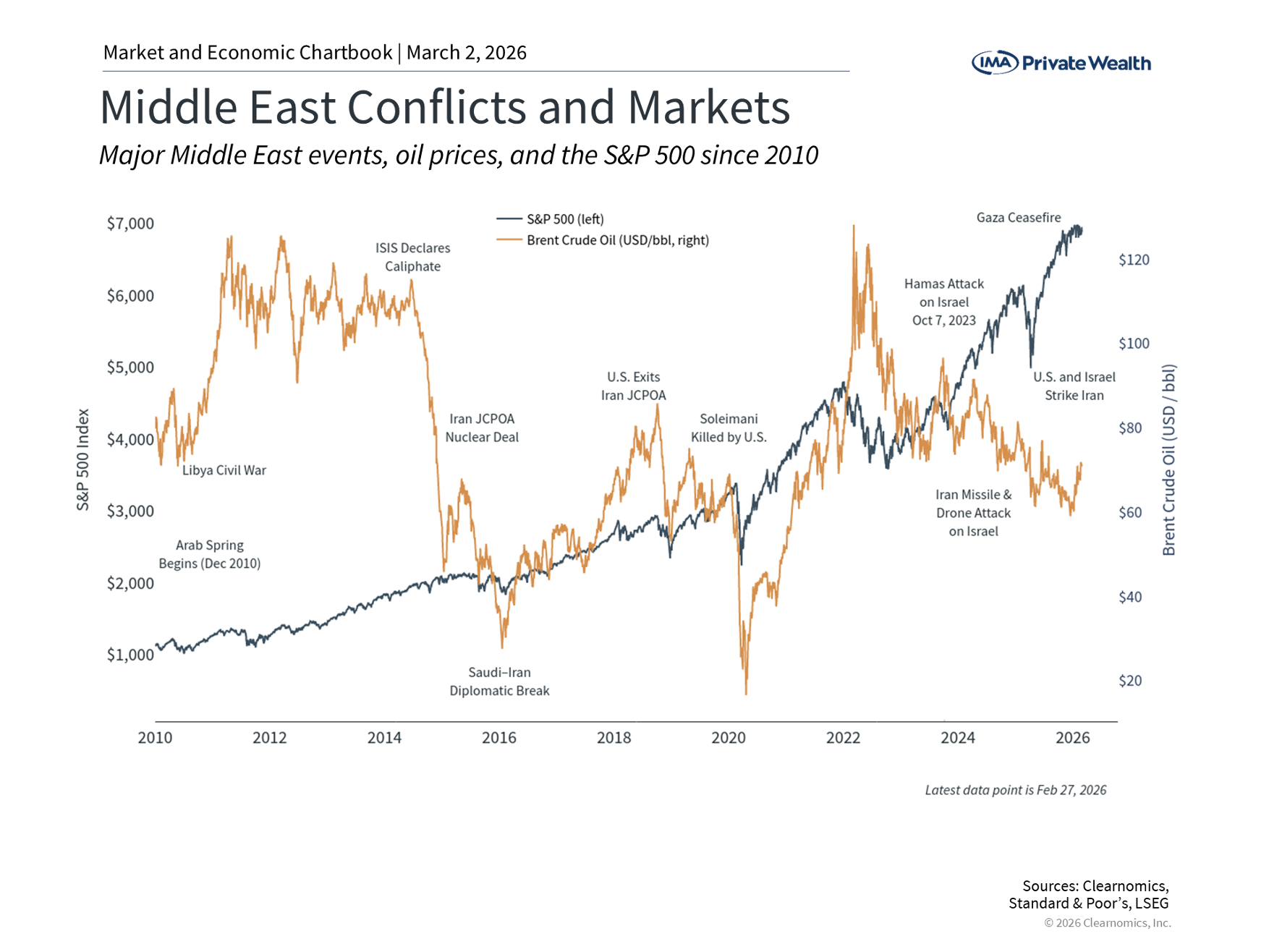

While the scale of the current strikes is significant, tensions between the U.S., Israel, and Iran have been escalating for some time. This latest development follows a monthlong U.S. military buildup in the region, negotiations over Iran’s nuclear program that failed to produce an agreement, and President Trump’s pledge to support Iranian protesters who challenged the regime earlier this year.

To understand how we arrived at this moment, it helps to consider the broader timeline of events:

The scope of the latest strikes, including the targeting of Iran’s senior leadership, is broader than previous engagements. However, history also makes it clear that these conflicts themselves are not always a catalyst for market movements.

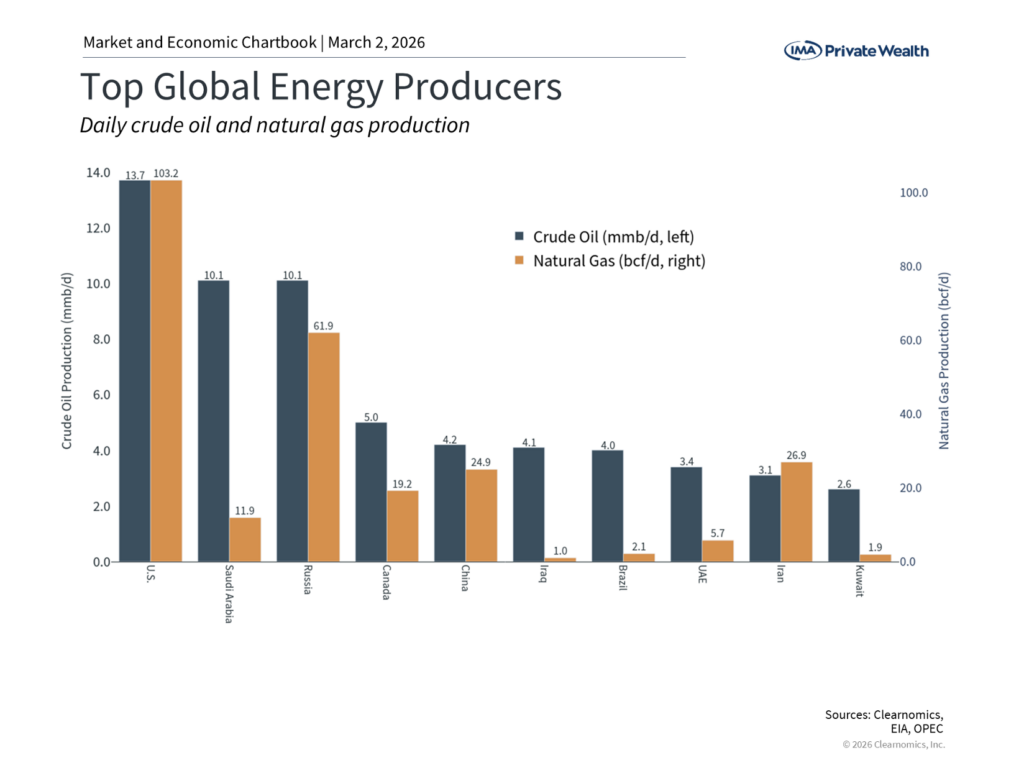

For investors, the most direct way that Middle East conflicts affect financial markets is through global energy prices. Iran is a member of OPEC and produces around 3 million barrels per day of oil, and 27 billion cubic feet per day of natural gas. The country also sits along the Strait of Hormuz, which is the world’s most critical energy waterway. According to the U.S. Energy Information Administration, approximately one-third of all seaborne oil exports and one-fifth of natural gas passes through this region. Even the threat of disruption to this critical waterway could have implications for global energy markets.

Oil prices had already been rising in anticipation of the strikes. The immediate reaction to the strikes has been a further jump in oil, to the low $70s for WTI and just under $80 for Brent crude. While western countries do not directly import oil from Iran, the fact that the market is global and oil is fungible means that any disruption to supply can raise prices.

However, some perspective is needed. Current oil prices remain well below the 2022 peak of nearly $128 per barrel when Russia invaded Ukraine. Today’s environment is quite different. In 2018, the U.S. also became the world’s largest producer of oil and natural gas, with current domestic production exceeding other major producers such as Saudi Arabia and Russia. While the U.S. still relies on global energy markets, this level of production helps to insulate the domestic economy from supply disruptions.

It’s also worth remembering that oil prices are hard to predict. When Russia invaded Ukraine, many expected prices to remain elevated indefinitely. Instead, prices stabilized and declined far sooner than projected. Similarly, the U.S. operation in Venezuela this past January led to a brief move in oil prices, but had little longer-term effect.

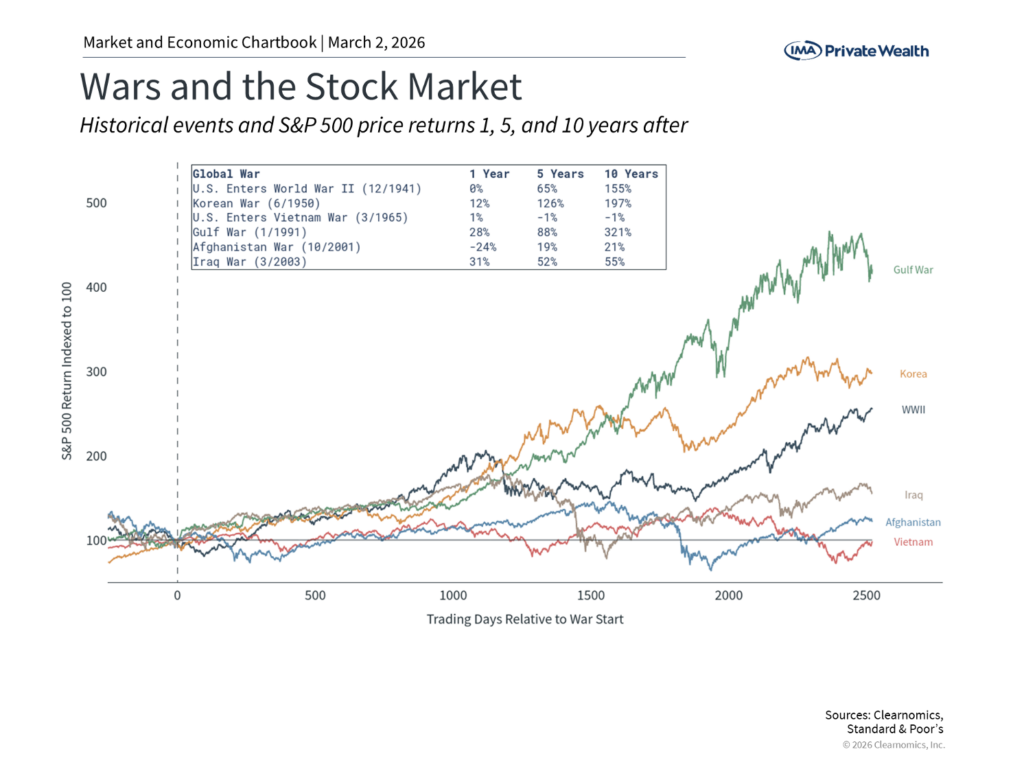

For long-term investors, the most important lesson from past geopolitical conflicts is the value of staying invested. It’s natural to feel uneasy when headlines describe military strikes, retaliatory attacks, and the possibility of a wider regional war. These events involve real human consequences and are unlike the typical flow of market news about earnings, valuations, and economic data.

The accompanying chart makes clear that markets have navigated even the most serious global events. From World War II to the Gulf War to the wars in Iraq and Afghanistan, markets experienced short-term volatility but were driven by economic fundamentals over the long run. More recently, the conflicts between Russia and Ukraine, and between Israel and Hamas, created uncertainty but did not derail the broader market trajectory.

It’s also important to note that Iran plays a minimal direct role in investment portfolios. Iran has been under heavy sanctions for years and its economy has been experiencing hyperinflation, with its currency, the Rial, collapsing. So, very few investors have direct exposure to the country in their asset allocations.

Markets may experience volatility in the coming days and weeks as the situation unfolds. Oil prices could rise further, and uncertainty could weigh on investor sentiment. But trying to time these moves has historically been counterproductive. Historically, markets have shown that they can rebound unexpectedly, and missing even a few of the best trading days can significantly reduce long-term returns.

The bottom line? The U.S. and Israeli strikes on Iran represent an important geopolitical development. However, history shows that investors who maintain diversified portfolios aligned with their long-term financial goals are best positioned to navigate periods of uncertainty.

Investment advisory services provided by IMA Advisory Services, Inc., (IMAAS). IMAAS is a federally registered investment adviser under the Investment Advisers Act of 1940 (CRD #112091). Registration as an investment adviser does not imply a certain level of skill or training. IMAAS is also a registered insurance agency. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. IMAAS Form ADV Part 2A and Form CRS can be obtained by visiting: https://adviserinfo.sec.gov and search for our firm name. Neither the information nor any opinion expressed is to be construed as solicitation to buy or sell a security of personalized investment, tax, or legal advice. IMAAS does business as IMA Private Wealth, IMA Retirement and Syntrinsic throughout the United States.

Forecasts of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. Assumptions, opinions, and estimates are provided for illustrative purposes only and are subject to significant limitations. Estimates are subject to uncertainty and error and could be significantly higher or lower than forecasted. They should not be solely relied upon as recommendations to buy or sell securities.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment or investment strategy will be profitable. Consult your investment, tax and legal advisors before making investments. IMAAS does not provide tax or legal advice.

The information in this document is not intended as a recommendation to invest in any particular asset class or strategy or as a promise of future performance. Given the complex nature of risk-reward trade-offs involved in portfolio construction, we advise clients to consult with their financial professionals on specific investment-related decisions. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. In addition, past performance is not a guarantee of future results.

Copyright (c) 2026 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

Before You File: What to Review and What to Plan Next

Apr 14, 2026

Before You File: What to Review and What to Plan Next

Apr 14, 2026

Understanding Market Volatility: What History Tells Investors

Apr 14, 2026

Understanding Market Volatility: What History Tells Investors

Apr 14, 2026

Understanding Trump Accounts: A New Approach to Saving for Children

Apr 7, 2026

Understanding Trump Accounts: A New Approach to Saving for Children

Apr 7, 2026

Conflict in Iran: What Rising Oil Prices Could Mean for Investors

Mar 25, 2026

Conflict in Iran: What Rising Oil Prices Could Mean for Investors

Mar 25, 2026